Following the news of the hurricanes, news of the Equifax security breach has been all over the news. Financial data of 143 million Americans has been stolen, and in many cases it means that the victims are at-risk of becoming victims of identity theft for the remainder of their lives. That’s right, you, and if you have them, your children, could be at risk for the rest of your life. The hackers got names, Social Security numbers, birth dates, addresses, credit card numbers, and some driver’s license numbers.

Following the news of the hurricanes, news of the Equifax security breach has been all over the news. Financial data of 143 million Americans has been stolen, and in many cases it means that the victims are at-risk of becoming victims of identity theft for the remainder of their lives. That’s right, you, and if you have them, your children, could be at risk for the rest of your life. The hackers got names, Social Security numbers, birth dates, addresses, credit card numbers, and some driver’s license numbers.

The breach ticks me off – this never should have happened. Clearly Equifax has some major vulnerability in their system which they should have known about and protected. A credit bureau should be utilizing the highest level of security at every level. Your information with them should be as secure as a vault. On top of that, to add insult to injury, three of Equifax’s executives (including the CFO) sold nearly $2 million worth of stock after the breach, but before they told the public about it. That’s right – here’s a timeline for you:

- Between mid-May and July, 2017 – breach happens

- July 29, 2017 – the hack was discovered

- Aug 1-2, 2017 – executives sell almost $2 million worth of stock

- Sept 7, 2017 – the public is informed of the breach (thank you, Equifax, for waiting more than a month before letting us know)

- Sept 8, 2017 – Equifax stock drops by double-digits

Equifax cliams that these executives had no knowledge of the hack when they sold their shares, but I don’t buy it. You’re telling me the CFO didn’t know about this? If he didn’t know, then who did? I’m sure that the timing of the sale will be part of any investigation.

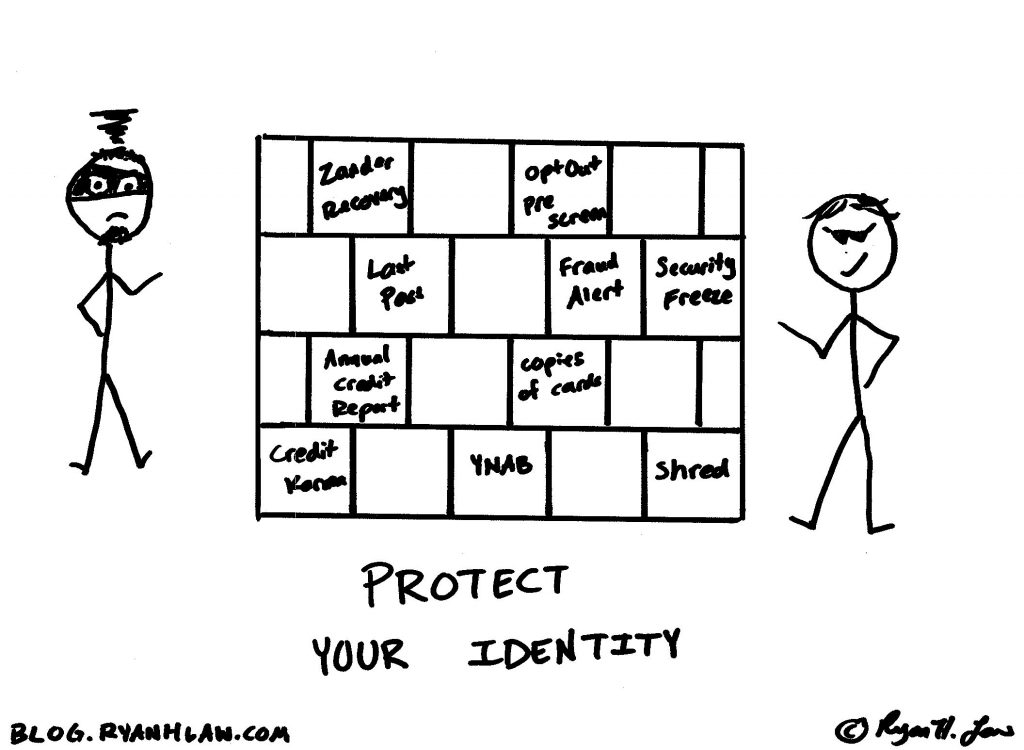

The breach has happened, though, and you need to take specific steps to be sure you protect yourself. Let me warn you now, the few hours you spend on this are not going to be the most fun, but it is critical you take care of it now. It will be much, much worse if you wait and are a victim of identity theft.

I’ll try to make it as easy as possible for you with links and instructions.

- First, don’t sign up for the protection that Equifax is offering. It’s garbage and only lasts a year, and, unless you opt-out of it, means you can’t be part of suing Equifax later on. I also don’t trust the company that just had the biggest data breach in history to be able to protect my data. Pass. Due to the severity of the breach, they should offer identity theft protection for life.

- Sign up for Credit Karma (https://www.creditkarma.com/). You will get free credit scores and free monitoring of your credit reports. If anything unusual happens, they will contact you. It’s a free service and you should sign up for all adult members of your family.

- Place a credit freeze on all three of your credit bureau files. A credit freeze is THE SINGLE MOST IMPORTANT THING YOU CAN DO TO PROTECT YOURSELF. It literally locks your credit bureau files so NO ONE, including you, will be approved for new credit. A thief could have your information and they will apply rapidly for credit, all of which will be denied. They will eventually move on. Depending on the state you live in, there will be a $0-$15 fee to set this up, and you need to do this for each adult member of your family.Here are the links:

https://www.freeze.equifax.com/Freeze/jsp/SFF_PersonalIDInfo.jsp

https://www.transunion.com/credit-freeze/place-credit-freeze

https://www.experian.com/freeze/center.htmlBecause millions of people are setting these up the systems are not all working. I was able to set up Equifax and Experian, but not TransUnion. I will keep trying throughout the next day or so, and if it doesn’t work I will take care of it via mail.If you need to apply for credit later, you can un-freeze your reports for a limited period of time, after which is will re-freeze.

- Place a fraud alert on your accounts. This is simply an extra step that puts an alert on your credit report that you might be a victim of identity theft, and that they need to call you before any transactions can be approved. It only lasts 90 days, but you can put the alert on there repeatedly. I already have a note on my calendar 90 days from today to renew the alert. You only need to place the alert with one company then they will place the alert with the other two. I recommend you use TransUnions fraud alert system – I found it to be the easiest one: https://www.transunion.com/fraud-victim-resource/place-fraud-alert

- Sign up for Zander Insurance identity theft insurance. For $145 a year it protects your entire family, including your children. They have a 100% recovery success rate and protect you against all types of ID theft, including tax fraud, medical ID theft, and, of course, financial fraud. If your identity is stolen as a result of the Equifax, or any other breach or identity theft, they will take over and fix everything. It is well worth every penny. You can sign up for that here: https://www.zanderins.com/idtheft2

![]()

- Speaking of children, does it make sense to freeze their reports? The credit bureaus don’t want you to be able to do that, but some states have made it mandatory. All three bureaus are falling in line, but none will allow you to do it online. TransUnion will do a search, for free, to see if your children have credit reports. You can find that here: https://www.transunion.com/credit-disputes/child-identity-theft-inquiry-form.

- Utah is taking things one step further – they have set up a Child Identity Protection Program through the Attorney General’s office that registers your children’s Social Security numbers as a number belonging to a minor, which will help protect their data. You can find that program here: https://cip.utah.gov/cip/SessionInit.action. If you live in a different state encourage your attorney general to create a similar program. Because I live in Utah and have this option, along with the Zander protection, I don’t feel that I need to freeze their credit, but if I lived outside of Utah I would absolutely take that step.

- Because credit card numbers were stolen, I recommend calling the toll-free number on the back of each credit card you have and requesting a new number. It’s a pro-active step you can take to prevent unauthorized charges in the future.

Again, I realize this isn’t fun – it’s a lot of work to set these things up, but I wouldn’t delay. Take a couple of hours today and get all of this done. Taking these steps is like building a brick wall between you and identity thieves.

Share this:

However, after a while, we got restless. We wanted to own a home. After all, that is the American Dream, right? So we started looking for homes. We found a brand new community that was being built, and they offered 100% financing. We picked out a home we liked and put down some earnest money, then they started building it. What an exciting time!

However, after a while, we got restless. We wanted to own a home. After all, that is the American Dream, right? So we started looking for homes. We found a brand new community that was being built, and they offered 100% financing. We picked out a home we liked and put down some earnest money, then they started building it. What an exciting time! Another red flag was that we had no money for a down payment or closing costs. Of course, to the seller, that was no problem. They could just roll it all in to the loan.

Another red flag was that we had no money for a down payment or closing costs. Of course, to the seller, that was no problem. They could just roll it all in to the loan.