Watch this first:

Identity theft really is a problem that affects millions of people each year. It causes untold numbers of hours and dollars to fix the problems.

While it is impossible to stop all identity theft, there are some simple steps you can take to protect yourself better.

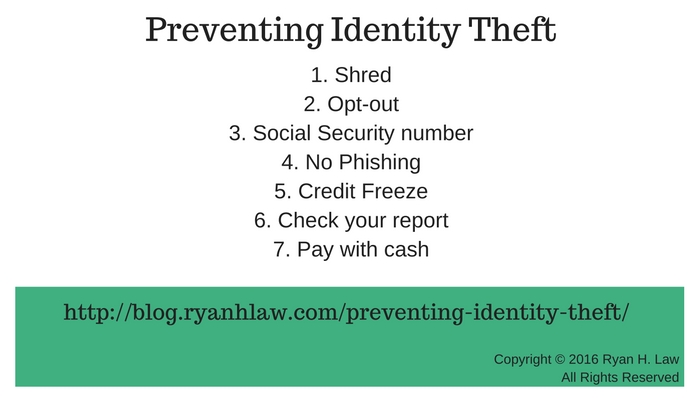

Shred Documents with Your Personal Information

You should shred any document from a financial institution, any pre-approved credit card offers, and any other documents with your personal information on it. Shredders that shred in long strips don’t work – thieves can tape together the strips (and will tape them together) and get your information or apply for credit. Some sites suggest simply tearing up and throwing away pre-approved credit card offers. Does that work? Check out this site for your answer:

http://www.cockeyed.com/citizen/creditcard/application.shtml

Use a cross-cut shredder to make sure it is fully destroyed.

Opt-out of Receiving Pre-Screened Credit Card Offers

On the website https://www.optoutprescreen.com/ you can opt-out of receiving pre-approved credit card offers. Eliminating these from your mailbox is one less thing for thieves to be able to steal.

Protect Your Social Security Number

Don’t carry anything with your Social Security number printed on it. Check your wallet or purse to see if you are carrying your social security card OR any other item with your Social Security number printed on it. Thieves really only need this one piece of information to steal your identity, so taking steps to keep it safe will help you keep your identity safe.

Don’t reply to “Phishing” E-mails

Never reply to e-mails for requests for any personal information, even if it looks like it is coming from your bank. Your bank will never request personal information via e-mail.

Put a Credit Freeze on Your Credit Report

One of the most effective things you can do to protect your identity is to freeze your credit. A credit freeze prevents the information in your credit file from being reported to anyone.

If a thief does steal your identity they can’t open new credit because your record is frozen. This will also prevent you from opening new credit unless you plan ahead and “unthaw” your credit report for a period of time. Credit freezes and unthaws do cost money, but think of the money spent like an insurance policy. Here are the websites to freeze your credit report:

https://www.freeze.equifax.com/Freeze/jsp/SFF_PersonalIDInfo.jsp

https://freeze.transunion.com/sf/securityFreeze/landingPage.jsp

http://www.experian.com/consumer/security_freeze.html

Check Your Credit Report

It is important that you check your credit report on a regular basis. You can get one free copy of each of your credit reports annually by visiting www.annualcreditreport.com. A strategy I use is to check one of the reports every 4 months – that way I am checking it out on a regular basis. If there are any errors or accounts you don’t recognize you need to take steps right away to get it taken care of.

Pay with Cash

A while back I got a call at 7:30 in the morning on a Saturday from the Fraud Department at my bank. My credit card number had been used for an online purchase that seemed uncharacteristic (it was a Jewish dating site), and the Fraud Department was calling to find out if my wife or I had used our card there. We had not, so they immediately closed down the card and issued a new number. When we tried to figure out how it happened we realized that the most likely scenario was when we used our debit card the last time we ate out. When the waiter/waitress takes your card and disappears with it for 2-3 minutes it is easy for them to snap a photo of the front and back using their cell phone. We now pay with cash anytime we eat out.

To review, you can help prevent identity theft I recommend that you:

- Shred documents with your personal information

- Opt-out of receiving pre-screened credit card offers

- Protect your Social Security number

- Don’t reply to “Phishing” e-mails

- Put a credit freeze on your credit report

- Check your credit report

- Pay with cash

What about identity theft insurance? Is it worth the cost? I’ll review what it is and my opinion about it in my next post.

By now you’ve probably heard about Wells Fargo and the $190 million fine they are being issued because their employees created more than 2 million unwanted deposit accounts and credit cards for their customers. Because of the scandal 5,300 employees have lost their jobs. Wells Fargo customers have paid hundreds of thousands of dollars in fees for these unwanted accounts.

By now you’ve probably heard about Wells Fargo and the $190 million fine they are being issued because their employees created more than 2 million unwanted deposit accounts and credit cards for their customers. Because of the scandal 5,300 employees have lost their jobs. Wells Fargo customers have paid hundreds of thousands of dollars in fees for these unwanted accounts.