Are you tired of watching your savings earn .02% per year and seeing your investments lose money each year? You’re not alone.

You probably feel a lot like this guy – you just want someone to “FIX IT!”

Let’s establish a few things up front:

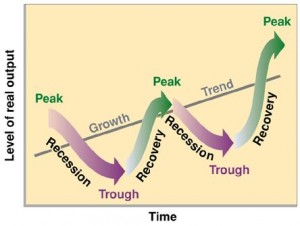

- The economy moves in cycles:

We go through times of high unemployment, low savings rates, negative stock market growth, etc. and we go through times of low unemployment, great stock market growth, etc.

It’s all part of a cycle.

There are times, of course, when the recessions and troughs last longer than others, but overall that is how the economy works. No one knows how long or short any part of the cycle is going to be.

- The “stock market” is made up of a lot of different components.

There are individual company stocks, company and government bonds and money market savings. It also includes things like commodities (gold and silver), oil and real estate. You can invest in all of these. - Most people invest in the stock market through their employer (401(k)) or through another retirement account such as an IRA. Typically this is in the form of mutual funds, which is a collection of corporate and government stocks and bonds. Throughout the article when I refer to investing in stocks I am talking about stock mutual funds. Most people shouldn’t be purchasing individual stocks.

- Past performance in the stock market doesn’t predict what it will do in the future, but it can give you an idea of trends.

So how do you make or lose money in the stock market? When the market is down in a recession or trough stocks generally lose money. This can be caused by many things. Most recently the drop in the market has been caused by economic issues in China and the low price of oil, along with a continuing sluggish economy in the U.S.

In the first two weeks of 2016 the stock market has lost about 8% of its value. 8% in two weeks! Everyone’s invested assets are taking quite a hit right now.

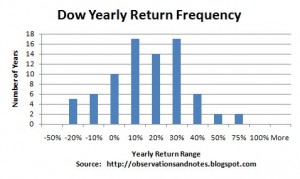

Let’s take a look at some historical data.

The graph above shows the Dow yearly return frequency. You can see that there are years that the return on your investments would have returned more than 70%, and years it would have lost more than 20%. About 25% of the time the market has lost money.

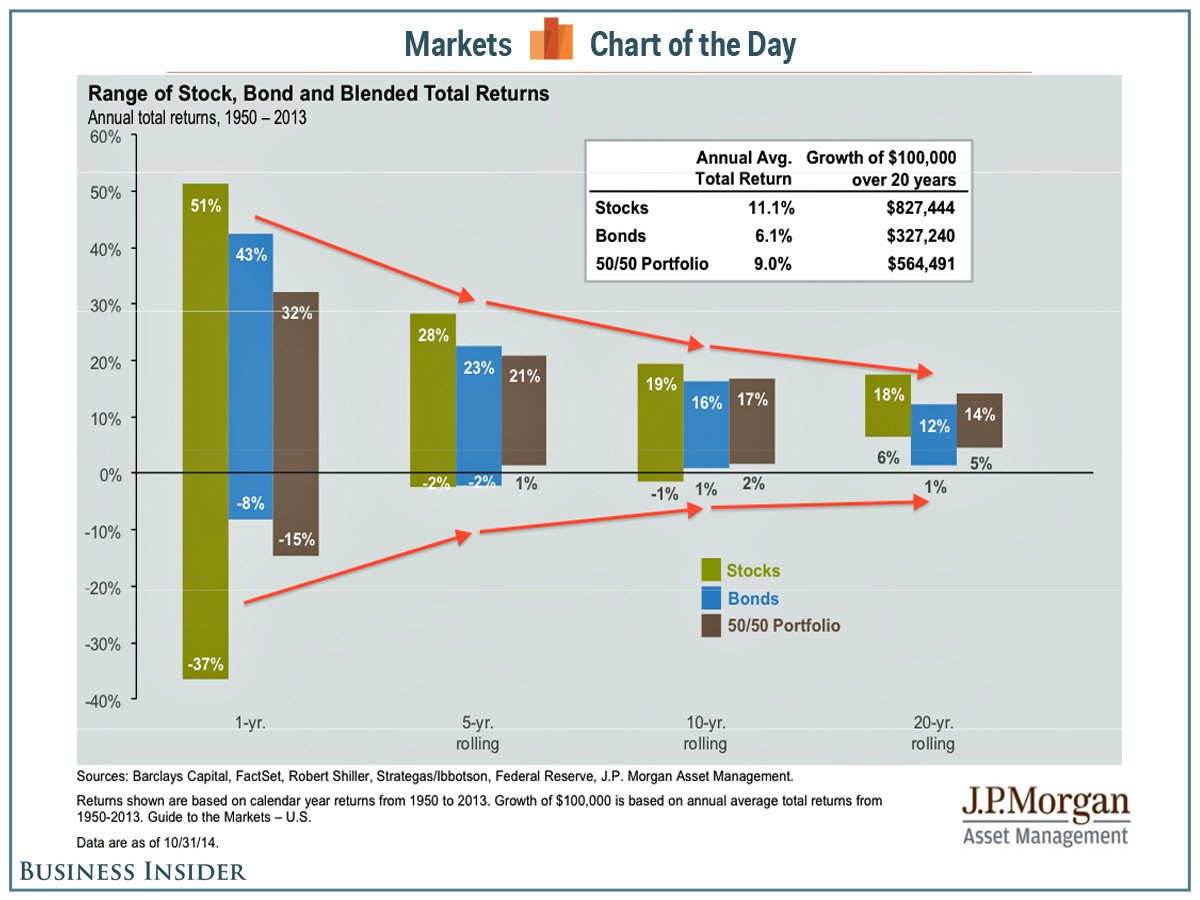

This next graph shows the range of returns for a portfolio of 100% stocks, 100% bonds and 50% stocks and 50% bonds between 1950-2013.

In a single year the stock portfolio returned between -37% and +51%.

If you invested for 5-years that range narrows to -2% and +28%

If you go out to 20 years, the range narrows even more to +6% and +18%.

The average annualized returns for stocks during those 20-year periods is 11.1%.

You have to decide if you are willing to ride out the negative years in hopes of gaining in the good years, and how long your time horizon is.

Here are some things to keep in mind:

- The further out your time horizon is the better chance you have of getting a positive return, with the stock market returning the most. If you don’t have at least 5 years, or even better 10 years, you shouldn’t be invested in stocks.

- The shorter your time horizon is the more you should be invested in conservative assets such as bonds. That means that you can be invested in stocks the younger you are, and move your money to bonds the closer you get to retirement.

- A good rule of thumb is that you should take 100 minus your age and that’s how much you should invest in stocks. If you are 40 years old you should invest about 60% in stocks (100 – 40 = 60%). If you are 55 years old you should invest about 45% of your money in stocks. Your risk tolerance level might be higher or lower than that, though. Here is a good free online tool that will help you determine your risk tolerance level: http://njaes.rutgers.edu:8080/money/riskquiz/. Because I have a higher risk tolerance I have more of my assets invested in stock mutual funds.

- Remember that there are additional ways to invest your money. While most of our retirement money is in the stock market, we are saving up money to invest in some real estate as well. A diversified portfolio is best.

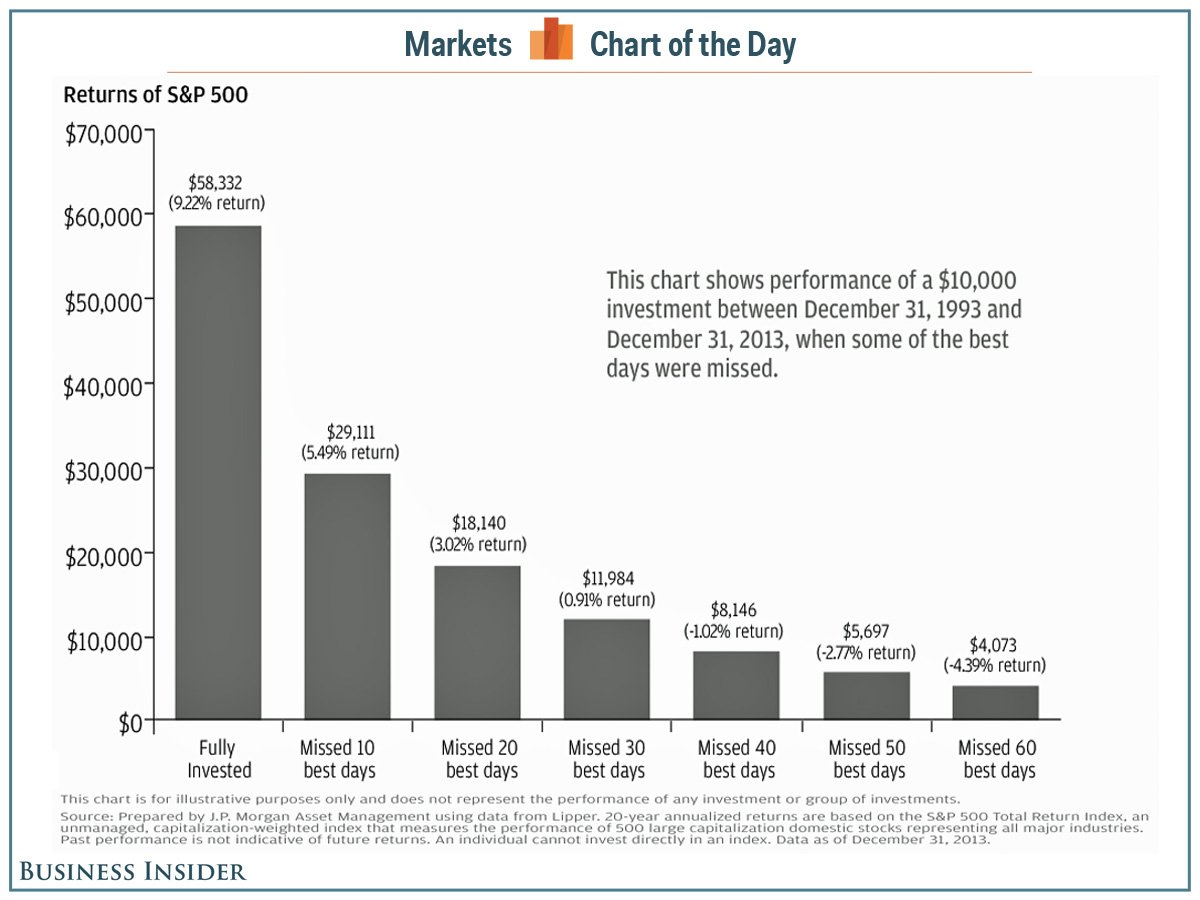

- What you don’t want to do is invest in stocks, panic when it goes down and pull all your money out, then when the market goes back up move your money back in to stocks. That’s a losing game, and you will never get ahead that way. You are buying high and selling low, which is the opposite of what you should do. A lot of people do this, however, which is why there is a big difference between investment returns and investor returns. Investment returns assume you leave the money in the market, while investors move their money around when things get bad.This chart helps me to remember that I need to stay invested:

This chart assumes you invested $10,000 between Dec 31, 1993 and Dec 31, 2013. During that time the stock market had some great years and rough years.If you kept it fully invested you would have ended up with just over $58,000. If you missed the 10 best days (which often come right after the worst days) your return drops to $29,000. If you missed the 40 best days your return is actually negative – your $10,000 drops to $8,147.

This chart assumes you invested $10,000 between Dec 31, 1993 and Dec 31, 2013. During that time the stock market had some great years and rough years.If you kept it fully invested you would have ended up with just over $58,000. If you missed the 10 best days (which often come right after the worst days) your return drops to $29,000. If you missed the 40 best days your return is actually negative – your $10,000 drops to $8,147.

People miss the best days all the time though because they switch from stocks to cash when the market goes down, miss the up-side, and invest when stocks are back at their most expensive.

I realize that all these charts and statistics don’t make you say, “Well, I’m sure glad my portfolio is losing money!” No one likes to see their portfolio drop for even a day, let alone for a few years in a row.

Every time it feels different, like we aren’t going to recover this time. I understand it. I get it. If you need help, find a financial planner who can help you set goals and stick to the strategy you outline together. Make sure it is someone you trust and has your best interests at heart. Someone who will teach you and encourage you and cheer you on.

As always, feel free to leave comments or ask questions below, on Facebook or in an e-mail.

Share this: