Your credit score plays a larger factor in your life than you might realize. For example, your credit score is a factor in:

- The rate you pay for loans

- The deposit you pay for utilities and your cell phone

- Your auto insurance

- Getting the job you want

- Getting into the apartment you want

In addition to all of these benefits of having a good score, monitoring your score regularly can also alert you to potential problems. If an account was opened in your name that you are not aware of, you could be a victim of identity theft.

There are several ways to monitor your score, but one method stands out due to its ease of use, how comprehensive it is, and the price (it’s free). That tool is Credit Karma.

Here is how Credit Karma describes their services:

Our goal is to help you understand your credit and get more out of it. Along with providing free credit scores, reports and monitoring, we offer insight into what it all means and show you product recommendations, like credit cards and loans, based on your credit profile.

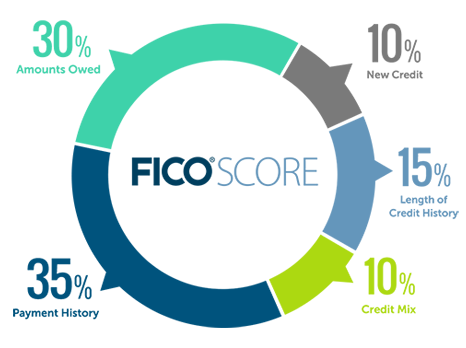

Basically they pull a copy of your credit report and scores from TransUnion and Equifax, and you can check it as often as you want (the website recommends weekly). You can then go in to detail about the six factors that determine your score (credit card utilization, payment history, derogatory remarks, age of credit history, total accounts and credit inquiries), along with recommendations for how to improve in that area.

For example, if the website shows that you have a poor ranking in credit card utilization you can click on that area and it will show how utilization is calculated, how much of a balance you are carrying on each card and several tips for improving in that area.

You can also run simulations to see how different scenarios would affect your score. For example, you can simulate what will happen to your score if you close a particular card, or pay your balances down or make a late payment.

Questions about Credit Karma

Is it secure?

Yes, it is secure. You do have to enter your social security number for them to be able to pull your report, but they take your data security very seriously. You can read about their security practices here: https://www.creditkarma.com/about/security.

Doesn’t pulling my credit hurt my score?

Yes and no. A hard inquiry (such as applying for a loan) does affect your score (only to a small degree, though). However, a soft inquiry does not. A soft inquiry is when you pull your own report, or your employer does, or a company like Credit Karma does. Reviewing your report and score on Credit Karma will have no effect on your score.

Will Credit Karma sell my information?

No. Their privacy policy restricts them from selling your information.

How is it free?

Credit card and loan companies pay for targeted advertising on the site. You will see recommendations specific to your situation and score. For example, when I logged in today it showed my four recommendations for credit cards, based on my credit score. I find their advertising very unobtrusive.

Check out Credit Karma today at https://www.creditkarma.com/.

NOTE: This will be the first in a series of articles about financial planning tools. I will review the tools that I have researched and use for my personal finances. If you have other tools you use to manage your money, please share them in the comments or in an e-mail.

Share this: